Strong Christmas sales: Lidl

Isolated locations: Co-op

Struggling: ASDA

The UK food industry is facing a period of chaos and change. At the beginning of the year, Wakefield-based Morrisons warned of extensive store closures and job losses. The group’s remaining fish, butchery and cheese counters are set to go, along with other added value categories. While Morrisons’ sales showed a 3.1% increase in the four weeks before Christmas, it is unlikely to prevent a fire sale of added value categories and a review of procurement priorities. The decline in the multiple’s commercial performance in recent months point towards a long term decline. So far this year, Morrisons has announced the closure of its Rathbones Bakery business, with a predicted 115 job losses: more can be expected to follow as the year progresses. It would be logical for middle grade management to be updating CVs and for senior management grades, along with board members, to be checking the scope of their their NDAs and how much wriggle room they have, if any, in the event of an unscheduled career move..

There are concerns, too, for the future of the Co-op.The chain has announced 19 store closures, which will be completed by the summer. Three sites will be leased out to B+M and the remaining 16 will be taken over by Sammy, a regional chain. The disposals will include stores in Norfolk, Leicestershire, the West Midlands, Nottingham and South Yorkshire. The Coop started the year with more than 2,200 outlets, many of them small, local supermarkets or c-stores. Closures would leave some significant gaps in the UK retail landscape and re-open questions over what can be considered viable. Like ASDA, the Co-op is struggling with significant debt problems and handed over its once thriving banking business to a debt management consortium. Given that Aldi is planning to open 80 stores over the next two years, it may be in a position to insist on favourable treatment when cherry picking underperforming sites from struggling competitors.

Christmas sales figures are still regarded as a long term indication of the profitability of retail businesses for the coming months. Tesco banked its largest surge in seasonal takings for December 2025, while Lidl, Sainsbury and Waitrose reported solid gains in December food sales. With a good number of retailers earning good margins with premium fresh food ranges, ASDA’s return to selling mainstram brands at discounted prices is a dated strategy. The return of Alan Leighton to his old firm suggests that the original problems were not addressed the first time round, which also begs the question of whether it will work the second time around. More than a generation after the original rollback, it is time to ask how many of the first rollback customers are still alive, let alone shopping for food. The ASDA demographic can be used to support a short to medium term reliance on brands with an appetite for older consumers, but the same data also makes a stronger case for building a strong rapport with younger consumers with young families. Younger customers would help to build a stronger future for the business, over a longer time span.

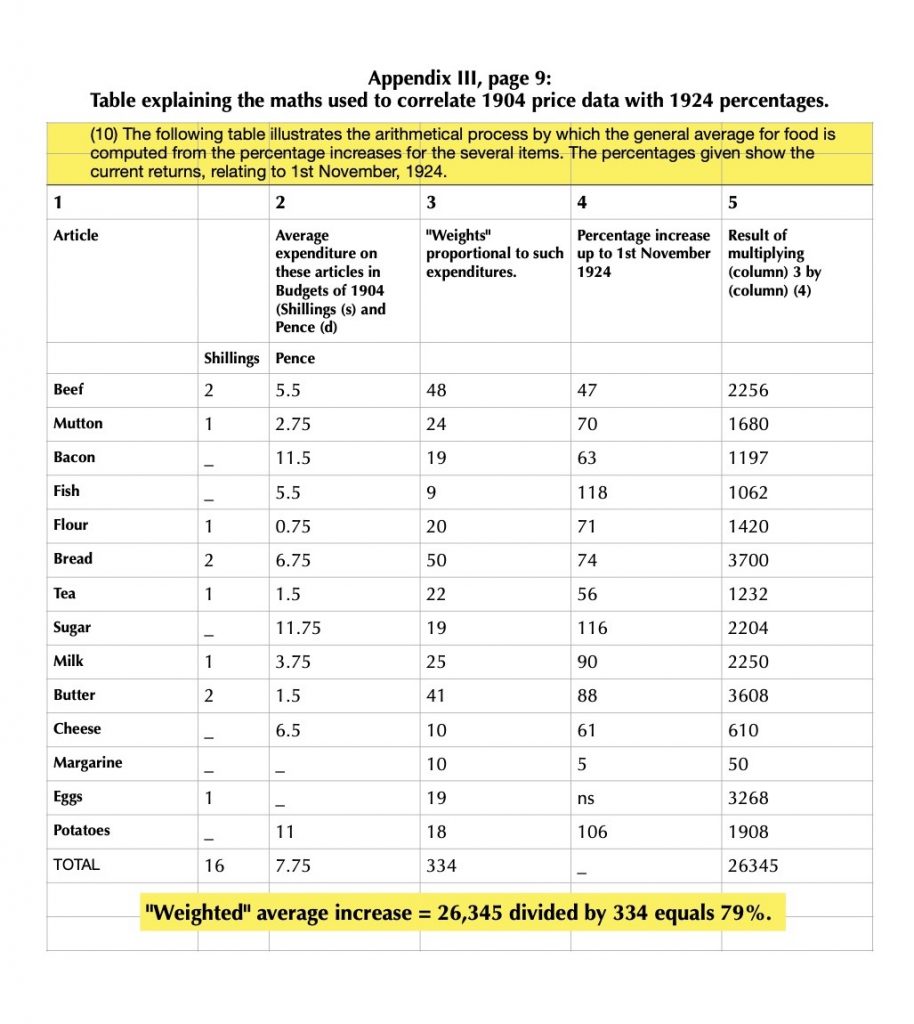

This could not come too soon, as inter-war businesses set about restoring their delivery systems. When trying to track the development of value in the pricing of bread and bakery goods, the editor of Industrial Peace, Major W Melville, conceded that the public grasp of the price structure was “little understood”. The only accessible estimates came from the Linlithgow Report and started outside bakeries with the purchase of sacks of flour. From the plains of north America, the vast expanses of Australia, to the more modest arable holdings of England, Linlithgow collects the entire growing stage of breadmaking flour into a single undifferentiated lump.

This could not come too soon, as inter-war businesses set about restoring their delivery systems. When trying to track the development of value in the pricing of bread and bakery goods, the editor of Industrial Peace, Major W Melville, conceded that the public grasp of the price structure was “little understood”. The only accessible estimates came from the Linlithgow Report and started outside bakeries with the purchase of sacks of flour. From the plains of north America, the vast expanses of Australia, to the more modest arable holdings of England, Linlithgow collects the entire growing stage of breadmaking flour into a single undifferentiated lump. The disadvantages of average returns are there for all to see. Melville put it like this: “No evidence offered in respect of price structure of flour. My inquiry begins at the point at which the baker buys his flour from the miller.” The opening price of breadmaking flour in January 1923 was 42 shillings and a penny. There is no indication of whether this should be taken as an “asking” price or a “taking” price, as given in a trade paper, meaning that flat pricing goes out of the window, speeded on its way by discounts applied at strategic order volumes. The figures discussed in the Linlithgow report were fixed during a time when flour prices were starting to fall, leaving a number of question marks over the validity of 42 shillings and a penny as a credible price for a sack of flour at this time.

The disadvantages of average returns are there for all to see. Melville put it like this: “No evidence offered in respect of price structure of flour. My inquiry begins at the point at which the baker buys his flour from the miller.” The opening price of breadmaking flour in January 1923 was 42 shillings and a penny. There is no indication of whether this should be taken as an “asking” price or a “taking” price, as given in a trade paper, meaning that flat pricing goes out of the window, speeded on its way by discounts applied at strategic order volumes. The figures discussed in the Linlithgow report were fixed during a time when flour prices were starting to fall, leaving a number of question marks over the validity of 42 shillings and a penny as a credible price for a sack of flour at this time.