Starting this month, food retailers across Britain face a new set of rules to ensure that pricing information is presented without exaggeration or distortion. This has been a running battle for trading standards officers for years, since supermarkets started tweaking their shelf displays to give them a stronger margin on own label products, leaving brands that already pay thousands of pounds every year in shelf money have to make do with low visibility facings and lost sales.

There is nothing new in this long-running argument, which has been running for about 15 years and was one of the reasons why the Grocery Commissioner was appointed in a bid to bring some order to the industry. Beter luck next time…

Next month town halls up and down the UK will be holding local elections. In past years, this multifaceted media matrix has not been covered in these pages. But this year, when the votes are counted, the distribution of political power across the landscape will change before a single committee meets or a single bin is emptied.

On May 7, voters will choose more than 4850 local councillors to run 134 local authorities. While the buildings will not look any different, the ways in which they will work will change literally overnight. Will the root causes of regional misunderstandings melt away in the warmth of a new dawn? The newly-constituted authorities will need to ensure funds remain available for local planning officials to have a better grasp of agricultural issues in their decision-making processes. Pigs might fly. Making waste disposal sites accessible and affordable can reduce the temptation to resort to fly tipping. Realistically, rural policing policy can only be based on lower population densities outside urban zones.

While canvassing for the local council elections, candidates can expect to face hostility on the doorstep on topics they have no control over. These could be items such as longer waiting lists for healthcare or services that voters believe to be cheaper/more reliable/generally favouring urban areas.

The lower density of rural populations made the provision online capacity less attractive for early commercial internet providers. Satellite services get round a lot of the transmission issues that faced early broadband services, butare not totally immune from signal issues, such as sunspots and solar flares. Sending a service engineer to repair a network outage in Dagenham can be covered by a simple phone call, while restoring an array of satellites takes some forward planning.

Tom Broadshaw has been speaking up for years to get fairer treatment for everyone in the supply chain.

Rather than accepting crumbs from the urban table, UK farmers need a market mechanism that protects their interests. For instance, as the law stands, farmers have no rights as suppliers to supermarkets. This fails to recognise the role food producers in mult-party supplier agreements, as well as being unfair. This particular bone of contention has been running for years now, NFU President Tom Bradshaw explained: “Farming is the backbone of our rural economy and lifeblood of rural communities. Our farmers manage over 70% of the landscape, protect enhance the environment and produce food for 70 million people.”

Confidence within the sector remains low. “Farm businesses are under extreme cost pressure, Bradshaw added. “Pressures for seed has been running high, fuel and fertiliser are exacerbated by geopolitical tensions,” he declared. Starting with the invasion of Ukraine and now the war in the Middle East, the political outlook is not predictable. Add it to the unstable climate and extreme weather and we all face problems that willimpact our ability to produce food.

“Decisions being taken by local authorities can have a direct and lasting impact on farm businesses and the communities they support. By championing pro-farming policies on areas such as planning, rural crime and the procurement of more British food, councils aren’t just supporting individual farming businesses — they can help turn the tide and shape the future of our industry by increasing our collective resilience.”

Once in a while, somebody releases statistics or data that tells a complete story in figures alone. Take this example from the National Farmers’ Union (NFU) last week.

…One fifth of laying hen are kept in sheds that are more than 25 years old, with the average shed age being 17 years. Meanwhile, sheds for pullet ands and breeding activities are even older . The total spend on building construction fell by 40% compared to the previous five-year period. The UK poultry sector is being squeezed, even if this is not immediately apparent.; If you want another example, many English pullets are living in sheds that are up to 50 years old, while their Welsh counterparts are accommodated in sheds that go back 12 years on average. (data available here))

There is no suggestion that the fabric of the buildings concerned could be unsound, but rather that as supermarket suppliers, they have faced pressure to leave capital expenditure for years on en. The lack of due process to recover their legitimate capital costs, let alone operating costs, just adds injury to insult.

DEFRA has announced changes to entry checks for High Risk Feed Not (of) Animal Origin (HRFNAO) They took effect on January 1.

Britain imports about half its food, and has been a food importer for centuries. As a collection of islands, the British Isles (which does not include Ireland, by the way) is vulnerable to naval blockades when at war. The same holds in peace time, when it makes sense to offer competitively-priced port facilities. The Brexit preparations included a charge for imported goods to drive off the ferry and cross the marshalling yard, to leave the port. This thinly-disguised daylight robbery is called the Common User Charge (CUC) and gives those people with power in the UK government an opportunity to harass port operators around the country, without having to own up scoring an own goal.

In its early drafts, the CUC was expected to cost £100 or less; then less than £150. Every time the CUC charges were modified or increased, the DEFRA civil servants cranked up their revenue expectations. Exporters to the UK had trouble finding out when the CUC would be coming into force and, more worryingly, what they could expect to pay to use British ports.

The UK has a very diverse port sector, owned and operated by all sorts of organisations and businesses. Trading structures with centuries of history rub shoulders with modern commercial operators. Take a port like Dover, the entry point for the lion’s share of the UK’s food imports.

The port was ganted a royal warrant in 1604 by James I, which transferred it to the town of Dover. It has been managed by a port trust ever since, until today it is one of the country’s largest ports.

Ever since James signed Dover’s royal warrant, the town has had a free hand to manage and operate its port facilities as it sees fit. The crown has been excluded from the site — and it would appear that the UK government deeply resents the status quo. In a spectacular display of ill ill, DEFRA has taken the opportunity to take a side swipe at the businesses that pay good money to use the port.

In mid-April, HMRC set a cat among the pigeons, announcing that CUC invoices would not be sent out until the end of July, just as the charge comes into force. Frantic enquiries from over-stretched company accountants went on to reveal that there would be no reference field on the CUC invoices that would enable invoices to be reliably checked against manifests before they are invoiced. To make matters worse, HMRC also informed importers that CUC invoices would revert to a four-week billing cycle, on July 30, when the first flush of CUC will also fall due, thereby engineering chaos for no good reason.

This deliberately provocative carry-on has fed a festering grudge. Like most ports run by a private trust in the UK, Dover is barred from using facilities and equipment as collateral when the port needs to raise money for capital investment. This requires an act of parliament. And a measure of tact.

This spring, Bradford-based supermarket chain Morrisons dumped all its added value satellite profit centres, in a bid to reduce costs and consolidate its position in the English groceries market.

The closures ensure that there can never be any question of a revival of the pipe dreams Morrison family shareholders entertained years ago. Morrisons was one of a number of retailers across Europe that monitored the twists and turns in the relations between Edouard Leclerc and the former Leclerc retail member Jean-Pierre Leroch.

Harassed andconstantly attacked bitterly by his former retail partner, Leroch established Intermarché, a retail group that owned the manufacturing capacity for 20% of its retail sales. This was successful in part due to the group’s strong roots in Britanny. The Intermarché business model was admired by many and bits of it were adopted by Swiss retailer Migros, as well as the Swiss Co-op and the Basque Eroski group.

The Morrison disposals are extensions of retail departments, such as the meat or fish counters, where higher levels of product knowledge are only retained at a price. The prospect of skilled staff moving to competitors is a bigger issue to operational management than it would ever be for strategic number crunchers. This has all the signs of a desperate attempt to throw heavy kit off a hot air balloon before it crash lands.

The further food travels, the more it should cost. Logically, yes, but the full story may not be quite so simple. With ingredients travelling literally half way round the world, it is no simple matter to differentiate one proposition from another. Take the example of 1925 loaf of bread, in the previous post. The starting point is 20-stone sack of flour that anyone could visualise for themselves, suppposedly costing 42 shillings and a halfpenny. There was, in those days, total silence from the millers concerning where their wheat came from, let alone what it might have cost. Since millers earn a living from making flour, their reticence is understandable.

By creating a synthetic starting point for the journey that would put a loaf of bread on the table, millers were able to influence the British public’s notion of what bread ought to cost. The 42 shilling sack was not a hard sell, it was a working price point for those years. However, the Linlithgow committee, to a man, refused to make any comment on the prices of wheat, wherever it might have come from. In one sense, wheat and bread pass through very different markets, yet the two are joined at the hip for some purposes, notably if supplies fail: no wheat, no flour, no bread. It is that simple.

All through the latter years of the nineteenth century, British ports were unloading grain from every corner of the known world. For most people, grain imports were a permanent fixture and, as part of the British Empire, this happy state of affairs would somehow be left continue. However, the U-boat attacks, which started in 1916, jolted Britain into protecting inbound shipments of any description. From being adventuresome and exciting, life on a long haul merchantman took on a more challenging aspect as the U-boats extended their range from the concrete bunkers at Rochefort, comfortably crossing the Bay of Biscay.

This female factory hand was photographed at work in Birkenhead during September 1918. Photo: Wikimedia Commons.

Logistics contractors refer to it as the final mile, but many of us would settle for “delivering the goods.” It is potentially a complex stage in a product’s journey to meet the end user.

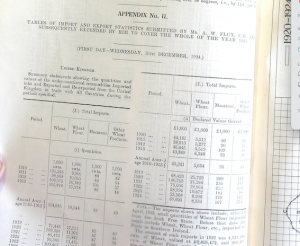

In December 1924, the LinLithgow Committee supplied the Royal Commission with four sets of operational models and an outwardly robust methodology to analyse the cost of bread. It was based on the bakers’ key ingredient, the 20-stone (127 kg) sack of flour at the heart of every batch of bread baked across the land in those days. In its day, this was a Known Value Item, to borrow a modern term. It traded at forty two shillings and a farthing, according to popular belief, not moving from one year to the next. Every baker who ever bought a sack of flour from a miller in those days paid 42s and one farthing, the story goes. Did anyone ever query the extra farthing? Where did it come from? Where did it go?

The biggest challenge that faces traders of all descriptions in arriving at a reliable price structure is the speed at which food products can change. Some animal products undergo a series of changes from farmgate to end user, others barely change at all. Some foods deteriorate very fast, while others are stable; add to this processes such as grading and the scope for differentiation can spiral out of control. For a comparison to be usable, the items need a number of similarities, bearing in mind that not all users will have the same interests. At the risk of keeping alive a business myth, there were some retailers who chose to take a cut in their margins rather than push up prices. Some individual members of of the Linlithgow committee would have been very well informed about specific markets and sector, but less inclined perhaps to share.

The stability and predictability of sectors such as cereal crops, milling and baking followed a pattern of incremental development. The step from wholesale trade to retailing, however, marks a sea change, reflecting the finer detail in retail distribution and home delivery costs. Investing in automotive resources ran deep in the bedrock of the economy of the day and was not going to be neither quick nor cheap.

The constant chivvying for market data was neither focussed for the most part nor available in the sort of unambiguous form that would have helped lay readers to learn more about the free market edifice. For instance, try explaining day-to-day shifts in retail pricing, arising from wholesale price changes that operate on a different basis. Even the denominations of coinage had an impact in the pricing of the retail world.

The ministry dug its heels in and refused to make a rod for its own back. The public should not be left to be baboozled by the high power antics of economists. How could such experts in their individual fields be left to explain the rise in mutton prices was a consequence of higher wool prices? After all, sheep are not killed for their wool.

The arrival of Vickers machine guns in the second Boer war changed military expectations of what would become possible in years to come.

Starting with the Boer war at the turn of the twentieth century, the impact of heavy machine guns was devastating on industrial battlefields, where thousands of horses were culled. The effect on the British economy was immense and immediate owing to the huge numbers of working animals needed to move equipment such as artillery from one site to the next. Such basic tasks became lethal interludes, as enemy machine gunners could take out the lead pair in a team of six or eight, immobilising the equipment, the surviving horses and the hapless soldiers who had to sort out the situation and salvage what was recoverable.

Horses and other pack animals were valued more highly by the British general staff than the rank and file soldiers of the day. The loss of thousands of horses was a problem for manufacturers everywhere, especially those who needed to provide local delivery services for their customers.

You can reckon that horses would have been expected to carry up to twenty percent of their body weight. Their harnesses may not have been taken into account, but would have been a significant proportion of the loaded animals’ burden. Establishing the loaded weight of a pack horse allows us to make some very rough and ready comparisons between the horses lost to the war effort and the rising numbers of two and three ton commercial vehicles that started to appear on British roads in 1914.

The power output of the early lorries used in opening years was fairly low for the most part, around 10 horsepower. You could say that every lorry did work that would have taken a team of six or a team of eight horses. In doing so, it is important to establish more than one set of parameters to make the comparison useable. It is fair to add that the power output from commercial motors increased rapidly from the late 1920s, this can readily checked by consulting contemporary advertisements. Despite its years of international power and influence, Britain was a net importer of horses between around 1860 and the 1930s. This not only stressed the economy, it makes valid comparisons between machinery and horses hard to establish.

It is quite likely that vehicle purchases made by the British government throughout the war years contributed to greater volumes of lorry traffic on British roads attributable to registered vehicles. Even if a high proportion of military vehicles are not registered through civilian agencies, what matters is that the total pool of vehicle tonnage was boosted in the process. Wartime government purchases of 20,000 vehicles will have added about ten million pounds to the postwar development iterations of the next generation of commercial motors..

The Departmental Committee on the Distribution and Prices of Agricultural Produce, generally referred to as the Linlithgow Committee, was proactive in its assessments and investigations of agricultural prices. Its remit covered the empire. The committee took its name from Victor Hope, 2nd Marquess of Linlithgow. He went on to chair a Royal Commission on food in India in 1928. Linlithgow, as the media called him, became the last viceroy of India: his 7-year tenure of office ended in 1943, amid scenes of chaos and civil unrest.

On December 11 1924, the second day of the 1925 Royal Commission, a senior MAF (Ministry of Agriculture and Fisheries) civil servant gave the government response to a raft of administrative measures recommended by the Linlithgow committee. Like a rabbit caught in car headlights, the MAF defence was more a limp lettuce than a fig leaf.

First up was a recommendation to standardise financial reporting for large companies such as United Dairies. MAF headed off further discussion, explaining that the government had “considered” introducing a bill, before playing its trump card: “The matter is now in the hands of the Board of Trade.” Next up, a suggestion that co-operative dairy schools should be revived is fended off with the assertion that a circular on the subject has been issued to all local authorities and “…steps are taken as opportunity offers.” Try getting that back out of the long grass.

The proposition that standing milk advisory committees should be set up to consider and discuss dairy industry issues as the need arose got short shrift. One of these bodies would cover Scotland, another would speak for the dairy industry in England and Wales: the topic prised about a dozen words from MAF: “Separate committees have been set up for England and Wales and for Scotland.” To finish the dairy section of the Linlithgow agenda, the committee urged the government to set and enforce minimum fat contents for whole milk cheese, cream and milk powder, which should apply both to imports and UK production. Sensing an imminent change of subject, the civil servant was more forthcoming. The health minister had made regulations that had come into force during May 1924. Meanwhile, the ministry of agriculture was: “…conducting investigations with a view to determining what standards, if any, may be adopted in respect of whole milk, cheese, and single and double cream.” Nothing gets past a pen pusher.

The Linlithgow committee and its extensive social network existed to promote the interests of landowner members. Its purpose was to develop a consensus around what constituted good practice, modern management and new routes to market. A fair proportion of these families would have benefitted from the compensation lavished on former slave owners: it never occurred to anyone that former slaves had a stronger case for reparations.

The Linlithgow committee (Lc) makes further recommendations, some of which I will list here, with MAF responses where relevant, including paras 258; 260; 302 and 303.

Para 258

Lc urges colleges and local authorities to train students in dairy production, as well as the prevention of spoilage. MAF agrees that this is worthy plan, even if some sites have needed assistance to reinstate standards.

para 260

Lc warns that whey is an ongoing problem, with little prospect of being profitable. MAF reports that a pilot plant has been transferred to Reading university, where development work is in hand.

The topic turns to commercial sharp practice: paras 209, 302 and 303. Since MAF replies to all these items in a single paragraph, I will add MAF’s response at the end of this post.

Lc is concerned that the practice of “averaging returns” is illegal and “not infrequent”. Growers should be checking all the entries on their invoices, the committee warned. Growers were not impressed. Another scam on similar lines started to rear its ugly head. By logging into the sales system under multiple identities, traders could cover their tracks and extract money from linked systems without being caught out.

Faced with significant numbers of food traders routinely breaking laws that may or may not have been enforceable in the first place, MAF resolutely turned its back and looked the other way:

“Efforts are being made to secure voluntary agreement between both sides of the industry on the points raised in their recommendations. If these efforts do not meet with success, it will be necessary to consider the introduction of legislation to deal with the points at issue.”

It would be reasonable to assume that it is the task of government to enforce existing laws and to review legislation that fails to meet the changing needs of the country. Accepting the status quo and asking both sides to play nicely in future resolves nothing. The problems will not go away without appropriate action; on the contrary, they will degenerate into crises.

For discussion of this theme in a more recent context, go to the contents page for France Loses Out and follow the links to individual topics.

More follows later: a series of related charts and some of the original text will be available in the near future.

“Decisions being taken by local authorities can have a direct and lasting impact on farm businesses and the communities they support. By championing pro-farming policies on areas such as planning, rural crime and the procurement of more British food, councils aren’t just supporting individual farming businesses — they can help turn the tide and shape the future of our industry by increasing our collective resilience.”

“Decisions being taken by local authorities can have a direct and lasting impact on farm businesses and the communities they support. By championing pro-farming policies on areas such as planning, rural crime and the procurement of more British food, councils aren’t just supporting individual farming businesses — they can help turn the tide and shape the future of our industry by increasing our collective resilience.” Once in a while, somebody releases statistics or data that tells a complete story in figures alone. Take this example from the National Farmers’ Union (NFU) last week.

Once in a while, somebody releases statistics or data that tells a complete story in figures alone. Take this example from the National Farmers’ Union (NFU) last week.

This spring, Bradford-based supermarket chain Morrisons dumped all its added value satellite profit centres, in a bid to reduce costs and consolidate its position in the English groceries market.

This spring, Bradford-based supermarket chain Morrisons dumped all its added value satellite profit centres, in a bid to reduce costs and consolidate its position in the English groceries market.