An unmistakeable sign of the impending holiday season turned up this morning in the form of an email from Thierry Jourdan, boss of the family-run cannery La Quiberonnaise in Britanny. Founded in 1921 by Thierry’s grandfather, the fish canning business packs sardines and mackerel landed by local inshore boats as well as taking in yellowfin tuna to pack a range of cans in domestic sizes.

Such canneries were a common sight in seaside towns during the first half of the twentieth century. Today, there are still a number of survivors in what used to be a crowded market. As the fleets dispersed and catches waned, the importance of the tourist trade was recognised by canneries along the French coast. The 1930s saw the establishment of paid summer holidays for French workers: it was the salvation of resourceful canners.

They greeted holidaymakers with open arms and tasteful souvenirs. Local artists are still engaged to create designs for annual editions of elaborately decorated cans of fish, with the promise of a fresh series the next year. Themes range from gently humorous picture postcard subjects to classical offerings that are as likely to end up in an art gallery as a kitchen. Canned fish as an art form has some unexpectedly well-known devotees. Food critic Jean-Luc Petitrenaud always takes a decorated can of sardines for his host whenever he is invited to dinner.

Total imports of Spanish olive oil to the UK topped 92,000 tonnes in 2021. That includes retail products, industrial, pharmaceutical, food manufacturing and UK-bottled own label product. The only tonnage it leaves out is olive oil sold by Lidl and Aldi. That represents a lot of demand for physical stock. Over the past decade it has climbed from 70,000 tonnes, with a wobble caused by high fuel prices in 2018.

The UK has been a strong market for olive oil in recent years, in a world where consumers are spending more than 14 and a half billion pounds a year on the Mediterranean’s most important crop. UK consumers will be paying rather more than their European neighbours in the coming months. They already pay over the odds, as it is.

The UK market caters for small introductory purchases: 250ml bottles currently retail for GBP 2.45p for olive oil, GBP 2.55p for EV (Sainsbury on June 1), while a Tesco 250ml bottle of bland mild and light olive oil has risen by 18% over the past year to GBP 2.83p. Tesco pricing for a litre of leading brand EV has risen steadily over the past 18 months by 50% from GBP 6.95p to GBP 10.40p, while ASDA increased the shelf edge price for the same branded litre of EV from GBP 6.50p to GBP 8 on June 1.

As of June 1, the ASDA shelfedge price for a one litre bottle of Filipo Berio EV went up to GBP 8, while Tesco was asking GBP 10.40 for the same product. It is safe to suppose that ASDA was not selling this line at a loss. So “every little helps” Tesco is charging 30% more than its rival. The day before, the differential was 60% for the same stock on the same shelves in their respective stores.

At a nearby town centre branch of Iceland during the same store check, the olive oil category was a one liner in every sense of the phrase. It comprised a single SKU, 500ml of ordinary olive oil for £4 in a tertiary brand, packed in a tidy plastic bottle. A no-frills distress purchase.

UK grocers selling olive oil have been milking the category. Spanish consumers get through a per capita average of 10 litres a year. They know what it’s worth and expect to get value for money. At the moment, headline olive oil prices are rising and are close to EUR 5,500 a tonne for EV grades. UK retailers will have to rethink their margin expectations if they are going to secure product and continue selling it. The party’s over, guys.

Goods that combine components from more than one trading bloc are subject to the Rules Of Origin procedure. Goods made in the EU are zero-rated on arrival in the UK, while the status of duty payable on third country components or ingredients used in EU goods is determined by applying Rules Of Origin. These establish whether or not the third country component has been transformed sufficiently for it to be considered an integral part of a new product. If it is a fellow traveller in a blended product, for instance, it is liable for duty.

The first target is to ascertain whether or not the component concerned has been absorbed into the finished EU product. If so, it can usually be covered by the duty payable on the finished product. If, on the other hand, it can be recovered from or identified within the EU product, the third country component may be liable for third country duty pro rata. The key marker is whether or not the third country component qualifies for a change of customs code. This will be decided by the UK customs staff on a case by case basis.

In the case of third country extra virgin olive oil (1509 2000), it is considered a fellow traveller in a blended product. This currently stands at 104 gbp per 100kg, according to the UK government online tariff service, https://www.trade-tariff.service.gov.uk/subheadings/1509200000-80 (as of check made on May 29).

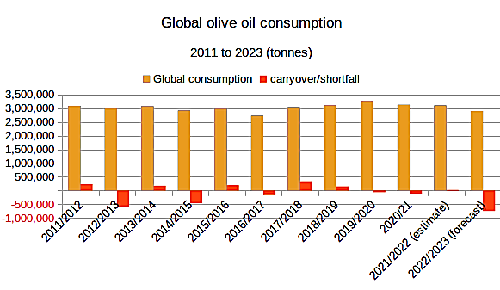

Spain, the world’s largest producer of olive oil, faces the prospect of running out of extra virgin olive oil in the coming months. According to industry figures seen by Urban Food Chains, forecasts for worldwide consumption of olive oil are expected to drop from 3.1 million tonnes to 2.9 million tonnes in the current campaign. There is a potential shortfall of 745,000 tonnes worldwide.

The Spanish industry invested heavily in extensive tree plantings around the turn of the century, with enough trees and crushing capacity to produce one and a half million tonnes of olive oil in a season. But the 2022-3 crop was a poor crop and down by over 50 percent against the previous campaign. This year a lot of flowers set on the trees, but like last year, the trees are stressed and are shedding the fruit.

With total olive oil stocks across the Spanish industry hovering at just over 607,000 tonnes, the sector faces empty tanks later this year. Domestic consumer demand is strong and April sales in Spain topped 63,000 tonnes. With at least six months to go before the next harvest comes onstream, Spanish consumers will be competing with exporters for physical stocks of olive oil.

Demand is strong and prices are high but expected to go up even further. Assuming that Spanish consumers ease up on their purchases of olive oil, which is not a given, a 5% drop in month on month sales volumes would represent a requirement of just over 277,000 tonnes between now and the next crop. The Spanish industry delivers shiploads of olive oil around the world and all over Europe by tanker truck. Exports as of around 50,000 tonnes a month would empty the country’s remaining stocks by November.

data source: International Olive Oil Coouncil

Like any other crop-driven commodity, there is a numbers game in play and prices will rise steeply to head off strong demand. Retail margins will come under pressure as physical product becomes harder to obtain. The EU has trade deals with north African producers, who can ship quota tonnages that member states can draw down with zero duty. Should any of this third country olive oil be packed for the UK market, even in a blended product, Rules Of Origin (ROO) would apply on arrival at the UK frontier, where duty would be charged on the non-EU content.

But the underlying concern has to be the drying out of water tables across a huge swathe of southern Europe and the Mediterranean basin. Olive trees have deep roots, but not deep enough, it might seem. In Spain, the planting of thousands of trees has propped up crop yields most years, but not all. This year’s forecast being a case in point.

The Groceries Code Adjudicator is tasked with ensuring fair play between market forces and retailers trying to manipulate things. There were many dubious practices in play at the end of the twentieth century and with retailers holding the whip hand over suppliers, an external agency was long overdue. The position of Groceries Code Adjudicator was first discussed in 2009 and it was long in the making. Its terms of reference are here. The Groceries Code Adjudicator Act of 2013 set up the retail watchdog, which operates out of one of London’s dockland office blocks.

Answerable to what was then the Department for Business, Energy and Industrial Strategy, the adjudicator had a handful of seconded secretarial staff. Just over a dozen retailers with annual sales of more than one billion pounds and now including Amazon, have compliance officers. These are members of the retailers’ management staff, charged with enforcing the provisions of the Act.

There is one major shortcoming with the framing of the act, though. While there are many links in a supply chain, only the retailer and the supplier who is paid by the retailer are covered by the legislation. As yet, there is no attempt to legislate for the more complex structures and working relationships that exist in the food industry.

Tesco has tried to revive shelf money for its online retail operation. At the end of the 2022-3 financial year the multiple announced its plan to impose two flat rate “fulfillment fees” : 12p/unit for branded goods, 5p/unit for own label lines. Short for Stock Keeping Unit (SKU), a unit is an item offered for sale. This incredibly blunt instrument was to be applied and charged to suppliers with threats of punitive retribution in the event of non-co-operation.

In practice it is not even remotely level-handed: suppliers of a £12 bottle of wine would face a one percent margin haircut, while companies supplying goods with a £1 price point face a 12 percent total margin wipeout. Not surprisingly, no-one is playing ball. The Grocery Code Adjudicator faces a major challenge, even though Tesco is out of order in this case. Watch this space.

NFU president Minette Batters told Urban Food Chains: “This move from Tesco is a stark demonstration of the lack of fairness within the supply chain. At a time when crippling production costs mean many farmers and growers can’t afford to continue producing food at scale, resulting in supermarket shortages of fruit, salads and eggs, the food industry desperately needs fairness and collaboration, not further erosion of trust.

The product descriptions that appear alongside customs codes in a schedule are set in stone. The whole point of the Harmonised System (HS) is that at any given time, specifications are the same from one trading bloc to the next. When classifying carcases, for example, there is no adjustment to be made for organic product over intensively-raised. The existence of additional input costs is of no concern when filling in customs declarations. Every market has its own mechanisms for assigning values and prices, which are separate from fiscal liability.

Travel often brings with it a taste for foods that consumers encounter while they are away from home. This broader view of food and drink gained momentum in the latter half of the 20th century, as shoppers started asking for avocado pears, a wider range of pizza and pasta products, not to mention a tidal wave of Asian foods that have been greeted with open arms and either adopted or adapted to British tastes. Many Indian foods have found their way to Britain over the centuries and some, like tea, became national institutions.

It is time to look at the historical context of moving food around the world and look at the topics of food security and self sufficiency. During the latter years of the twentieth century, Britain was about 50% self sufficient: the official headline figure was closer to 65%, but since UK food manufacturers import a variable proportion of their ingredients, these shipments should be taken into account. The impact of two world wars on the domestic economy of Britain leaves a residual malaise and feeling that the UK “…ought to do better…” at producing its own food, notably among older generations.

There is an array of variables that define the economic environment in which food is produced, some of which can be covered now. The first is the colonial plantation paradigm in which overseas territories are ruled and exploited solely to produce commodity crops for colonial powers. Britain, Holland, Spain and Portugal come to mind as historic colonisers, shipping plant material and slave labour in to strategic locations, usually between the tropics. Feeding the work force was a low priority, but was usually a part of the operational model.

Down the intervening centuries this practice continued, developing into what is now referred to as landgrabbing. The topic is extensively documented by Fred Pearce, author of The Land Grabber. The 2012 book can be bought as a paperback or a download here. As the name suggests, land is bought or leased and fenced off. This has been practiced by countries such as China and a number of Arab states. The enclosed land is brought into cultivation usually by nationals from the states concerned and the crops are shipped to these countries as they are harvested. Local populations are excluded from these holdings, which are often of the highest quality available locally.

While this is a modern, pernicious practice, it is not without historical precedent. Irish Quaker and philanthropist Joseph Fisher was a poor law commissioner during the Irish potato famines of the 1840s. From his family home, overlooking the approach to Cork harbour, Fisher recalled seeing ships setting sail bound for English ports. These vessels were laden with grain grown and harvested by starving labourers in the surrounding counties. Fisher went on to write the 1865 book Where Shall We Get Meat? As it happened, shiploads of cheap grain started crossing the Atlantic, as the American railroad system reached the eastern seaboard and started a sea change in European livestock sectors. The entire history of North America to that point is itself dominated by a high profile land grab in which indigenous American peoples were marginalised by settlers and farmers.

The buying power of remote markets can have an immediate impact on the food security of rural populations. This is a measure not of aggregate harvests, but their availability for local communities.

Despite the inference that there could be multiple options, being a third country is a binary opposite of a member state in European parlance. The possible source of ambiguity in this distinction is that there are two implied alternatives to being a third country. Between themselves, EU member states use the term third country to refer to countries which are not EU members, in much the same way a verb might be conjugated. To complete the analogy, the first person is the member state speaking, the second person refers to the other member states on an equal footing, while the third person is identified as a separate, external non-member.

Unlike other areas of European policymaking, in which a wide spectrum of buying-in is accepted without argument, the distinction between being a member state and a third country is fundamentally indivisible. The UK negotiators failed to gain any traction in their attempts to carve out a halfway quasi-membership status that might have opened the way to feathering a cuckoo’s nest of a la carte patronage for British interests. The choice of Michel Barnier to lead Brexit talks for the European Union reflected his commitment to the indivisible membership of a European community that was used to accommodating consensus policymaking in specific areas and contexts.